As confidentially submitted to the Securities and Exchange Commission on July 26, 2021.

This draft registration statement has not been publicly filed with the Securities and Exchange

Commission and all information herein remains strictly confidential.

Registration No. 333-_____

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT UNDER SECURITIES ACT OF 1933

TC BIOPHARM (HOLDINGS) LIMITED 1

(Exact name of registrant as specified in its charter)

| Scotland | 8731 | Not Applicable | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

Maxim 1, 2 Parklands Way

Holytown, Motherwell, ML1 4WR

Scotland, United Kingdom

+44

(0) 141 433 7557

(Address, including zip code, and telephone number, including

area code, of Registrant’s principal executive offices)

TC BioPharm (North America) Inc.

C/o Business Filings, Inc.

108 West 13th Street

Wilmington, Delaware 19801

(800) 981-7183

(Name,

address, including zip code, and telephone number,

including area code, of agent for service)

Copy of all communications including communications sent to agent for service, should be sent to:

Andrew D. Hudders, Esq. Golenbock Eiseman Assor Bell & Peskoe LLP 711 Third Avenue – 17th Floor New York, NY 10017 (212) 907-7300 ahudders@golenbock.com |

Joseph Lucosky, Esq. Lucosky Brookman LLP 101 Wood Avenue South 5th Floor Iselin, NJ 08830 (732) 395-4402 jlucosky@lucbro.com |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is an emerging growth company.

| Emerging Growth Company [X] |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. [ ]

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | Proposed

maximum aggregate offering | Amount of Registration Fee | ||||||

| Ordinary shares, £1.00 par value (2)(3) | $ | $ | ||||||

| Representative’s warrants (3) | $ | - nil | $ | -nil | ||||

| Ordinary shares, issuable upon exercise of the representative’s warrants (2)(4) | $ | $ | ||||||

| Total fee | $ |

| (1) | Estimated solely for purposes of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended, or the Securities Act. Includes the offering price of ordinary shares that the Underwriters have the option to purchase to cover over-allotments, if any. |

| (2) | In addition, pursuant to Rule 416 under the Securities Act of 1933, as amended (“Securities Act”), the securities being registered hereunder include such indeterminate number of ordinary shares as may be issuable with respect to the ordinary shares being registered hereunder as a result of stock splits, stock dividends or similar anti-dilutive transactions. |

| (3) | No additional registration fee is payable pursuant to Rule 457(g) under the Securities Act. |

| (4) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(g) under the Securities Act. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

1. We intend to alter the legal status of our company under Scottish law from a private limited company immediately prior to completion of this offering by re-registering as a public limited company and changing our name from TC Biopharm (Holdings) Limited to TC Biopharm (Holdings) plc. See the section titled “Corporate Reorganization” in the prospectus which forms a part of this registration statement.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED JULY __, 2021

PRELIMINARY PROSPECTUS

____ Ordinary Shares

TC BIOPHARM

This is the initial public offering of ordinary shares of TC BioPharm (Holdings) Limited. All of the ordinary shares are being sold by us.

Prior to this offering, there has been no public market for our ordinary shares. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to apply to list our ordinary shares on The Nasdaq Global Market under the symbol “ ____ .” No assurance can be given that our application will be approved or that an active trading market for our ordinary shares will develop.

We are a “foreign private issuer,” and an “emerging growth company” each as defined under the federal securities laws, and, as such, we will be subject to reduced public company reporting requirements. See the section entitled “Prospectus Summary—Implications of Being an Emerging Growth Company and a Foreign Private Issuer” for additional information.

Investing in our ordinary shares involves a high degree of risk. See “Risk Factors” beginning on page 13 for a discussion of information that should be considered in connection with an investment in our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial public offering price | $ | $ | ||||||

| Underwriting discounts and commissions (1) | $ | $ | ||||||

| Proceeds to us (before expenses) | $ | $ | ||||||

(1) In addition, we have agreed to reimburse the underwriters for certain expenses not exceeding $_____ and issue warrants to the representative of the underwriters, or the Representative, in an amount equal to ___% of the aggregate number of ordinary shares sold in this offering, or the Representative Warrants. See the section titled “Underwriting” beginning on page 119 of this prospectus for additional disclosure regarding underwriter compensation and offering expenses.

We have granted the underwriters an option to purchase from us, at the public offering price, up to ____ additional ordinary shares, less the underwriting discounts and commissions, within 45 days from the date of this prospectus to cover over-allotments, if any. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable will be $____ , and the total proceeds to us, before expenses, will be $_____ .

The underwriters expect to deliver the ordinary shares to purchasers in the offering on or about _____________, 2021.

EF HUTTON

division of Benchmark Investments, LLC

The date of this prospectus is ______ , 2021

TABLE OF CONTENTS

| 2 |

Neither we nor the underwriters have authorized anyone to provide information different from that contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectus prepared by us or on our behalf. Neither we nor the underwriters take any responsibility for, and can provide no assurance as to the reliability of, any information other than the information in this prospectus, any amendment or supplement to this prospectus, and any free writing prospectus prepared by us or on our behalf. Neither the delivery of this prospectus nor the sale of our ordinary shares means that information contained in this prospectus is correct after the date of this prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy these ordinary shares in any circumstances under which such offer or solicitation is unlawful.

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us or to which we have referred you. We or the underwriters have not authorized anyone to provide you with information that is different. We and the underwriters are offering to sell the ordinary shares, and seeking offers to buy the ordinary shares, only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the ordinary shares.

For investors outside of the United States: Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to this offering and the distribution of this prospectus outside the United States.

Unless the context requires otherwise, in this prospectus TC BioPharm (Holdings) Limited and its subsidiaries (“Subsidiar(y/ies)”), “TC BioPharm (Holdings) plc,” and “TC BioPharm” shall collectively be referred to as “TCB,” “the Company,” “we,” “us,” and “our” unless otherwise noted. Prior to completion of this offering, we intend to re-register TC BioPharm (Holdings) Limited as a public limited company and to change its name to TC BioPharm (Holdings) plc and adopt articles of association in compliance with the laws of Scotland. See “Description of Share Capital and Governing Documents” for additional information about the proposed terms of the articles of association.

This prospectus includes our audited consolidated financial statements as of and for the fiscal years ended December 31, 2019 and 2020 prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). We refer to these consolidated financial statements collectively as our “annual consolidated financial statements.” None of our financial statements were prepared in accordance with U.S. GAAP. Our financial information is presented in pounds sterling. For the convenience of the reader, in this prospectus, unless otherwise indicated, translations from pounds sterling into U.S. dollars were made at the rate of £1.00 to $1.3662, which was the noon buying rate of the Federal Reserve Bank of New York on December 31, 2020. Such U.S. dollar amounts are not necessarily indicative of the amounts of U.S. dollars that could actually have been purchased upon exchange of pounds sterling at the dates indicated. All references in this prospectus to “$” mean U.S. dollars and all references to “£” and “GBP” mean pounds sterling. Our fiscal year begins on January 1 and ends on December 31 of the same year. All references to fiscal year 2019 relate to the year ended December 31, 2019 and fiscal year 2020 relate to the year ended December 31, 2020.

We have made rounding adjustments to reach some of the figures included in this prospectus. As a result, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that precede them.

This prospectus includes statistical, market and industry data and forecasts which we obtained from publicly available information and independent industry publications and reports that we believe to be reliable sources. These publicly available industry publications and reports generally state that they obtain their information from sources that they believe to be reliable, but they do not guarantee the accuracy or completeness of the information. Although we believe that these sources are reliable, we have not independently verified the information contained in such publications. In addition, assumptions and estimates of our and our industry’s future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause our future performance to differ materially from our assumptions and estimates.

Some of our trademarks and trade names are used in this prospectus, which are intellectual property owned by the Company. This prospectus also includes trademarks, trade names, and service marks that are the property of other organizations. Solely for convenience, our trademarks and trade names referred to in this prospectus appear without the TM symbol, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights, or the right of the applicable licensor to these trademarks and trade names.

| 3 |

ENFORCEABILITY OF CIVIL LIABILITIES

TCB is a corporation organized under the laws of Scotland. Substantially all of TCB’s assets and its directors and executive officers are located and reside, respectively, outside the United States. Because of the location of TCB’s assets and board members, it may not be possible for investors to serve process within the United States upon TCB or those persons with respect to matters arising under the United States federal securities laws or to enforce against TCB or persons located outside the United States judgments of United States courts asserted under the civil liability provisions of the United States federal securities laws.

TCB understands that there is doubt as to the enforceability in Scotland and the United Kingdom, in original actions or in actions for enforcement of judgments of United States courts, of civil liabilities predicated solely upon the federal securities laws of the United States insofar as they are fines or penalties. In addition, awards of punitive damages in actions brought in the United States or elsewhere may be unenforceable in Scotland and the United Kingdom by reason of being a penalty.

TCB has appointed TC BioPharm (North America) Inc., a Delaware corporation, its wholly owned subsidiary corporation, located at Business Filings, Inc. 108 West 13th Street, Wilmington, Delaware 19801 as its agent to receive service of process in any action against it in any state or federal court in the State of New York.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

TCB discusses in this prospectus its business strategy, market opportunity, capital requirements, product introductions and development plans and the adequacy of the Company’s funding. Other statements contained in this prospectus, which are not historical facts, are also forward-looking statements. TCB has tried, wherever possible, to identify forward-looking statements by terminology such as “may,” “will,” “could,” “should,” “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates” and other comparable terminology.

TCB cautions investors that any forward-looking statements presented in this prospectus, or that TCB may make orally or in writing from time to time, are based on the beliefs of, assumptions made by, and information currently available to, TCB. These statements are based on assumptions, and the actual outcome will be affected by known and unknown risks, trends, uncertainties and factors that are beyond its control or ability to predict. Although TCB believes that its assumptions are reasonable, they are not a guarantee of future performance, and some will inevitably prove to be incorrect. As a result, its actual future results can be expected to differ from its expectations, and those differences may be material. Accordingly, investors should use caution in relying on forward-looking statements, which are based only on known results and trends at the time they are made, to anticipate future results or trends. Certain risks are discussed in this prospectus and also from time to time in TCB’s other filings with the Securities and Exchange Commission (“SEC”).

This prospectus and all subsequent written and oral forward-looking statements attributable to the Company or any person acting on its behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. The Company does not undertake any obligation to release publicly any revisions to its forward-looking statements to reflect events or circumstances after the date of this prospectus.

| 4 |

The following summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information you should consider before investing in our ordinary shares. You should carefully read this prospectus in its entirety before investing in our ordinary shares, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

The Company

Corporate Overview

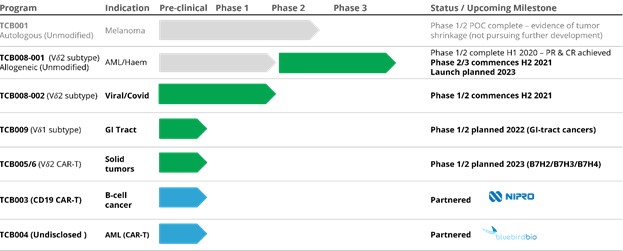

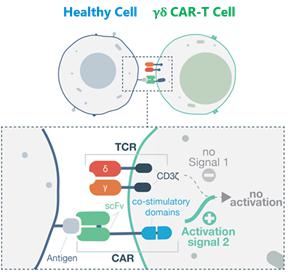

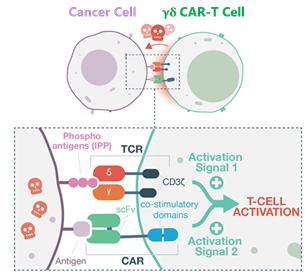

TCB, a private limited company based in Scotland, is a clinical-stage biopharmaceutical company focused on developing novel immunotherapy products that are based on our proprietary allogeneic gamma delta T (abbreviated as GDT) cell platform. Harnessing the innate ability of GDTs has enabled TCB to develop a range of clinical-stage cell therapies designed to combat identified cancers and viral infections.

TCB is embarking on phase II-into-pivotal (phase III) clinical studies, which is expected to commence in the fourth quarter of 2021, following United Kingdom and European Union regulations, with a view to launching its first oncology product, which will be for the treatment of acute myeloid leukemia (abbreviated as AML). We plan to conduct similar clinical trials in the United States in 2022 following a planned application to the FDA. Clinical results generated thus far have enabled TCB to obtain FDA orphan drug status for its method of treatment of AML.

In addition to unmodified allogenic GDTs for treatment of blood cancers, TCB also is developing an innovative range of genetically-modified chimeric antigen receptor modified T cells (abbreviated as CAR-T) products for treatment of solid cancers. TCB believes that solid cancers are more difficult to treat than blood cancers and may require addition of a chimeric antigen receptor (abbreviated as CAR) to (i) help therapeutic cells ‘navigate’ into diseased cancerous tissue, and (ii) retain therapeutic cells in-situ at the lesion for maximum efficacy.

In response to the recent pandemic, because GDTs are natural killers of virally infected cells, as well as cancerous cells, TCB is planning clinical studies to treat with both acute and long term COVID-19 symptoms. We believe acute COVID-19 studies will be undertaken starting in the fourth quarter of 2021.

Patent Portfolio and Intellectual Property

We believe TCB has a strong portfolio of patents and licenses covering the manufacture and commercialization of GDT cell products and their modification via CAR-T. We own one granted patent and 47 patent applications in six families, and have an exclusive license to an additional one family of 14 patents. We protect our proprietary position, generally, by filing an initial priority filing at the United Kingdom Intellectual Property Office, or UKIPO, followed by patent applications under the Patent Co-operation Treaty claiming priority from the initial application(s) and then progressing to national applications in, for example, the United States, Europe, Japan, Australia, New Zealand, India and Canada.

As a platform technology, we believe the co-stimulatory CAR-T-GDT cell system has a wealth of potential options to build added functionality. We plan to continue to innovate and partner in the field to augment our drug products and introduce next generation attributes. We will also continue to innovate our manufacturing and supply chains to efficiently scale our processes and simplify the interface with patients and healthcare professionals, whilst continually seeking to reduce manufacturing costs to improve patient access.

We intend to continue building on our technology platform, comprised of intellectual property, proprietary methods and know-how in the field of GDT cells. These assets form the foundation for our ability, not only to strengthen our product pipeline, but also to successfully defend and expand our position as a leader in the field of cell-based immuno-oncology.

Our Product Strategy

Our strategic objective is to build a global therapeutic business with an extensive portfolio of the two principal sub-types of GDT (GDT D1 & GDT D2) cell-based products with the potential to significantly improve the outcomes of patients with cancer and infectious disease.

Our strategy is to take a step-wise approach to clinical development and commercialization. After our inception, we made clinical transitions from autologous GDTs to allogeneic GDTs to CAR-modified allogeneic GDTs. Our commercialization strategy is to introduce clinical studies for products firstly in blood cancers (AML initially) and then solid tumor indications in the 2022 and 2023 timeframe. The latter will initially be focused on gut-related solid cancers. Complementarily, since GDT cells are dysfunctional in patients with severe viral diseases, TCB plans to commence development of treatment for COVID-19, with phase I/II clinical studies in the EU commencing in the fourth quarter of 2021, with predicted efficacy data available in the first half of 2022, and thereafter co-develop the COVID-19 treatment with one or more pharmaceutical companies for phase II/III studies and later commercialization.

| 5 |

Since 2015, TCB has maintained medicinal product manufacturing facilities for Investigational Medicinal Products MIA (abbreviated IMP), operated under license from the United Kingdom Medicines and Healthcare Products Regulatory Agency (abbreviated MHRA). In April 2016, the MHRA granted a ‘Specials’ license to TCB, which allows it to treat patients under supervision of a qualified doctor outside a clinical trial, and approved the company’s facility for ongoing Good Manufacturing Process (“GMP”) compliance, which permits the manufacture and release of Advanced Therapy Medicinal Products (abbreviated ATMPs) for use in clinical trials. TCB maintains a rigorous Quality Management System, which is based on the principles of the current GMP of the European and UK law and regulation and EudraLex Volume 4, as revised. The Company complies with the two directives laying down principles and guidelines of GMP for medicinal products were adopted by the Commission. Directive 2003/94/EC applies to medicinal products for human use and Directive 91/412/EEC for veterinary use. Detailed guidelines in accordance with those principles are published in the Guide to Good Manufacturing Practice which will be used in assessing applications for manufacturing authorizations and as a basis for inspection of manufacturers of medicinal products.

Regulatory approval of all aspects of medicinal therapy development, testing, manufacture and commercialization always is of concern. In the case of treatment for AML, TCB has developed the novel approach of antibody-based immunotherapy and adoptive cell therapy with the aim to improve anti-leukemia T cell function. Therefore, TCB is able to take advantage of orphan medicine regulation provided by the European Medicines Agency (abbreviated EMA) and the United States Federal Drug Administration (abbreviated FDA), which are designed to encourage medicine development for small numbers of patients where there is little commercial incentive under normal market conditions.

Part of our strategy is to collaborate with appropriate partners. We have a relationship with NIPRO Corporation (Osaka, Japan), both as a strategic investor and in collaboration to carry our certain proof of concept work in relation to GDT therapies. TCB also has a collaboration with bluebird bio, inc. (Cambridge, Massachusetts, USA) to advance our CAR engineered products into clinical development in multiple cancer antigens.

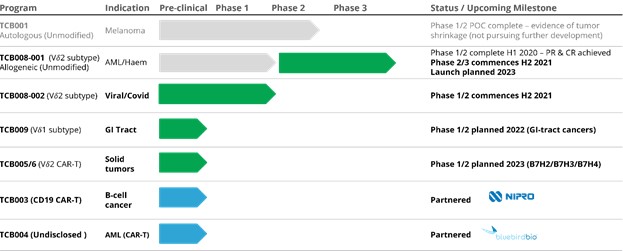

Our current products in our pipeline are:

Our unmodified cell therapy, used in the treatment of Acute Myeloid Leukemia (Program TCB008-001), is supplied under the name OmnImmune; and our unmodified cell therapy, used to treat COVID-19, is supplied under the name ImmuniStim.

TCB’s Strengths

TCB believes it has certain identified strengths. These include:

| ● | Clinical trials that have provided strong evidence of safety and clinical benefit; | |

| ● | A proprietary co-stimulatory CAR-T technology platform which we believe allows solid cancers to be treated without toxic side-effects; | |

| ● | Identification of a large pool of cancer targets for which we believe we can develop therapeutic candidates; | |

| ● | Retention of key business elements, including the manufacture and clinical research of our products; | |

| ● | Robust, and growing intellectual property portfolio protecting our products and proprietary platform; |

| 6 |

| ● | Our policy of developing strategic collaborations with leading, international companies to work together with us to develop certain GDT CAR-T products into clinic. We believe that existing and future collaborations will provide us with experience in scale-up and automation, and post-authorization sales and marketing; | |

| ● | A highly knowledgeable and experienced management team with extensive industry experience and expertise in the United States and in Europe; and | |

| ● | Ability to treat of patients under the ‘Specials’ regulatory framework in Europe and the United States. |

Corporate Information

Our principal executive offices are located in Scotland, United Kingdom, with a mailing address of Maxim 1, 2 Parklands Way, Holytown, Motherwell, ML1 4WR, United Kingdom and our telephone number at that location is +44 (0) 141 433 7557. Our website address is https://www.tcbiopharm.com/. The information contained on, or that can be accessed through, our website is not part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

Corporate Reorganization

Prior to the completion of this offering we will undertake a corporate reorganization pursuant to which TC BioPharm (Holdings) Limited will become the direct holding company of TC BioPharm Limited and will re-register as a public limited company and change its name to TC BioPharm (Holdings) plc. Pursuant to the terms of the corporate reorganization, the shareholders of TC BioPharm Limited will exchange each of the shares held by them in TC BioPharm Limited for the same number and class of newly issued shares of TC BioPharm (Holdings) Limited and, as a result, TC BioPharm Limited will become a wholly owned subsidiary of TC BioPharm (Holdings) Limited. In addition, all of our outstanding series A ordinary shares and ordinary shares will convert into a single class of ordinary shares and following such conversion shall be governed in accordance with the terms of our articles of association. Please see “Corporate Reorganization” in this prospectus for more information.

Implications of Being an “Emerging Growth Company”

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act. As such, we are eligible to, and intend to, take advantage of certain exemptions from various reporting requirements applicable to other public companies that are not “emerging growth companies” such as not being required to comply with the auditor attestation requirements in the assessment of our internal control over financial reporting of Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act. We could remain an “emerging growth company” for up to five years, or until the earliest of (a) the last day of the first fiscal year in which our annual gross revenue exceeds $1.07 billion, (b) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of our ordinary shares that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (c) the date on which we have issued more than $1 billion in nonconvertible debt during the preceding three-year period.

Implications of being a “Foreign Private Issuer”

We are subject to the information reporting requirements of the Securities and Exchange Act of 1934, as amended, the Exchange Act, that are applicable to “foreign private issuers,” and under those requirements we file reports with the SEC. As a foreign private issuer, we are not subject to the same requirements that are imposed upon U.S. domestic issuers by the SEC. Under the Exchange Act, we are subject to reporting obligations that, in certain respects, are less detailed and less frequent than those of U.S. domestic reporting companies. For example, we are not required to issue quarterly reports, proxy statements that comply with the requirements applicable to U.S. domestic reporting companies, or individual executive compensation information that is as detailed as that required of U.S. domestic reporting companies. We also have four months after the end of each fiscal year to file our annual report with the SEC and are not required to file current reports as frequently or promptly as U.S. domestic reporting companies. Our officers, directors and principal shareholders are exempt from the requirements to report transactions in our equity securities and from the short-swing profit liability provisions contained in Section 16 of the Exchange Act. As a foreign private issuer, we are not subject to the requirements of Regulation FD (Fair Disclosure) promulgated under the Exchange Act. In addition, as a foreign private issuer, we are permitted to follow certain home country corporate governance practices instead of those otherwise required under the Nasdaq Stock Market rules for domestic U.S. issuers and are not required to be compliant with all Nasdaq Stock Market rules as of the date of our initial listing on Nasdaq as would domestic U.S. issuers These exemptions and leniencies will reduce the frequency and scope of information and protections available to you in comparison to those applicable to a U.S. domestic reporting company. We intend to take advantage of the exemptions available to us as a foreign private issuer during and after the period we qualify as an “emerging growth company.”

| 7 |

The Offering

The following is a brief summary of certain terms of this offering.

| Ordinary shares offered by us | _____ ordinary shares | |

| Ordinary shares outstanding before this offering | ___________ ordinary shares | |

| Ordinary shares to be outstanding after this offering | ____ ordinary shares (or ___ ordinary shares if the underwriters exercise in full their option to purchase additional shares) | |

| Over-allotment option | The underwriters have an option for a period of 45 days to purchase up to _____ additional ordinary shares to cover over-allotments, if any. | |

| Representative’s warrants | We will issue to the Representative warrants to purchase up to ______ ordinary shares (or ______ ordinary shares if the underwriter exercises its over-allotment option in full). The warrants will have an exercise price of _____ % of the per share public offering price, will be exercisable on the date of issuance and will expire five years from the effective date of the registration statement of which this prospectus forms a part. | |

| Use of proceeds | We estimate that the net proceeds from our issuance and sale of ordinary shares in this offering will be approximately $ million, assuming an offering price of $ per ordinary share, the midpoint of the estimated price range of the ordinary shares set forth on the cover of this prospectus, and after deducting underwriting discounts and commissions and offering expenses payable by us. If the underwriters exercise the over-allotment option in full, we estimate that the net proceeds from this offering will be approximately $ million, assuming an offering price of $ per ordinary share, and after deducting underwriting discounts and commissions and offering expenses payable by us.

We currently expect to use the net proceeds from this offering primarily to finance the cost of treating patients under our proposed clinical trials TCB 008-001 (a phase II/III trial for the treatment of acute myeloid leukemia) and TCB 008-002 (for the treatment of COVID-19 infections) and to continue the research and development of our proposed GD-T CART therapies to treat sold cancers, as well as financing our operating overhead costs.

The exact amounts and timing of these expenditures will depend on a number of factors, such as the timing, scope, progress and results of our research and development efforts, the timing and progress of any partnering efforts, and the regulatory and competitive environment.

See “Use of Proceeds” on page 50 of this prospectus for more a complete description of the intended use of proceeds from this offering as well as “Risk Factors.” | |

| Risk factors | You should read the “Risk Factors” section starting on page 13 of this prospectus for a discussion of factors to consider carefully before deciding to invest in our securities. | |

| Proposed Nasdaq trading symbol | We intend to apply to list the ordinary shares on the Nasdaq Global Market under the symbol “_____.” No assurance can be given that a liquid trading market will develop for the ordinary shares in the United States. |

The number of our ordinary shares to be outstanding immediately after this offering is calculated taking into account the re-registration of company as a public limited company from being a limited liability company, under the name TC BioPharm (Holdings) plc, with reference to our entire issued share capital of ______ ordinary shares as of ______, 2021. The foregoing amount gives effect to the conversion, immediately prior to the completion of this offering, of all issued and outstanding ordinary shares, Class A ordinary shares, conversion of the _____ convertible notes and issuance of ordinary shares under the ____ Share Option Plan and assumes the additional issuance of _______ ordinary shares pursuant to the adjustment provisions in the Class A ordinary shares.

| 8 |

Unless otherwise indicated, all information in this prospectus, including information relating to the number of ordinary shares to be outstanding immediately after the completion of this offering excludes:

| ● | Any exercise by the underwriters of the over-allotment option or of the warrant to purchase up to ordinary shares (or ordinary shares if the underwriters exercise in full their option to purchase additional ordinary shares) to be issued to the Representative in connection with this offering. | |

| ● | Any exercise of options granted under our employee share option plan or other option grants or rights to purchase shares described in this prospectus. | |

| ● | Any additional shares to be issued to the holders of our A Ordinary Shares in connection with their rights to receive additional shares upon conversion of A Ordinary Shares into Ordinary Shares in certain circumstances described in our Articles of Association. |

Unless otherwise indicated, all information in this prospectus assumes no exercise by the underwriters of the over-allotment option and no exercise of the warrant to purchase up to ordinary shares (or ordinary shares if the underwriters exercise in full their option to purchase additional ordinary shares) to be issued to the Representative in connection with this offering.

Except as otherwise indicated references to our articles of association in this prospectus, unless the context provides otherwise, refer to our articles of association as currently expected to be in force for TC BioPharm (Holdings) plc immediately before the completion of this offering.

| 9 |

Summary Consolidated Financial Data

We prepare our consolidated financial statements in accordance with IFRS as issued by the IASB. The following summary historical consolidated financial data as of and for the years ended December 31, 2019 and 2020, have been derived from our audited consolidated financial statements, which are included elsewhere in this prospectus. Our historical results for any prior period are not necessarily indicative of results expected in any future period.

The financial data set forth below should be read in conjunction with, and is qualified by reference to, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and notes thereto included elsewhere in this prospectus.

We maintain our books and records in Pounds Sterling (£), and we prepare our financial statements in accordance with IFRS as issued by the IASB. We report our financial results in pounds sterling. For the convenience of the reader, we have translated pound sterling amounts in the tables below as of December 31, 2020, and for the year ended December 31, 2020, into U.S. dollars at the noon buying rate of the Federal Reserve Bank of New York on December 31, 2020, which was £1.00 to $1.3662. These translations are solely for illustration and convenience and should not be considered representations that any amounts have been, could have been or could be converted into U.S. dollars at that or any other exchange rate as of that or any other date.

| Year Ended December 31, | ||||||||||||

| 2019 | 2020 | 2020 | ||||||||||

| (in thousands, except per share data) | ||||||||||||

| Consolidated Statement of Comprehensive Loss: | ||||||||||||

| Revenue | £ | 3,427 | £ | 1,979 | $ | 2,703 | ||||||

| Research and development expenses | (8,614 | ) | (6,680 | ) | (9,126 | ) | ||||||

| Administrative expenses | (3,015 | ) | (2,207 | ) | (3,015 | ) | ||||||

| Other income | 1,561 | 569 | 778 | |||||||||

| Finance income - interest | 22 | 1 | 1 | |||||||||

| Finance costs | (275 | ) | (292 | ) | (399 | ) | ||||||

| Loss before tax | (6,894 | ) | (6,630 | ) | (9,058 | ) | ||||||

| Income tax credit | 826 | 1,172 | 1,601 | |||||||||

| Net loss for the year | (6,068 | ) | (5,458 | ) | (7,457 | ) | ||||||

| Total other comprehensive income/(loss) | - | - | - | |||||||||

| Total comprehensive loss for the year | £ | (6,068 | ) | £ | (5,458 | ) | $ | (7,457 | ) | |||

| Basic and diluted loss per share | £ | (3.39 | ) | £ | (2.88 | ) | $ | (3.93 | ) | |||

| Weighted average shares outstanding | 1,792 | 1,892 | ||||||||||

| As at December 31, | ||||||||||||

| 2019 | 2020 | 2020 | ||||||||||

| (in thousands) | ||||||||||||

| Consolidated Statement of Financial Position items: | ||||||||||||

| Cash and cash equivalents | £ | 956 | £ | 748 | $ | 1,022 | ||||||

| Working capital (1) | 336 | (1,970 | ) | (2,691 | ) | |||||||

| Total assets | 10,140 | 7,267 | 9,928 | |||||||||

| Total liabilities | (12,679 | ) | (10,614 | ) | (14,500 | ) | ||||||

| Share capital and share premium account | 12,877 | 16,542 | 22,600 | |||||||||

| Accumulated deficit | (15,416 | ) | (19,889 | ) | (27,173 | ) | ||||||

| Total equity attributable to the equity shareholders of the parent | (2,539 | ) | (3,347 | ) | (4,573 | ) | ||||||

| (1). | Working capital is defined as current assets less current liabilities |

| 10 |

Our business is subject to a number of risks and uncertainties, including those risks discussed at-length in the section below titled “Risk Factors.” These risks include among others the following:

| ● | We have generated operating losses since inception and expect to continue to generate losses. We may never achieve or maintain profitability. We will continue to require financing to continue to implement our business plan. | |

| ● | We, as well as our independent registered public accounting firm, have expressed substantial doubt about our ability to continue as a going concern. | |

| ● | Our lack of any approved products and our limited operating history may make it difficult for an investor to evaluate the success of our business to date and to assess our future viability. | |

| ● | GDT cell therapies are a novel approach to treating cancers and viruses, which have development risks and will require us to obtain regulatory approvals for development, testing, commercialization, manufacturing and distribution. We may not achieve all the required regulatory approvals or approvals may not be as timely as needed. | |

| ● | Because of the novel approach, potential side effects, and long-term efficacy, regulatory approval will require considerable time for trials, data collection, regulatory submissions and funding for the process. | |

| ● | Enrolling patients in clinical trials me be difficult for many reasons, including high screen failure, GDT cell proliferation capacity, timing, proximity and availability of clinical sites, perceived risks, and publicity about the success or lack of success in the methods of treatment. Covid 19 requirements may also disrupt or delay the conduct of clinical trials. | |

| ● | Because GDT cell therapies are novel, our research and development, and clinical trial results may not support our products intended purposes and regulatory approval. We are heavily dependent on the success of our lead product candidates, TCB008-001, TCB008-002, TCB005. TCB006 and TCB009. | |

| ● | Market opportunities for certain of our product candidates may be limited to those patients who are ineligible for or have failed prior treatments. This class of patient may be limited in number, difficult to locate and service, require special governmental approval, and unable to pay or obtain reimbursement. | |

| ● | We rely on many third parties for aspects of our product development and commercialization, such as raw material supply, clinical trials, obtaining approvals, aspects of manufacturing, development of additional product candidates and distribution. We may not be able to control these parties and their business practices, such as compliance with good manufacturing requirements or their ability to supply or service us timely, which will likely disrupt our business. | |

| ● | We face substantial competition: others may discover, develop or commercialize competing products before or more successfully than TCB. | |

| ● | Even if we are able to commercialize any product candidates, such drugs may become subject to unfavorable pricing regulations or third-party coverage and reimbursement policies. Commercialized products may not be adopted by the medical profession. | |

| ● | Because we are operating internationally, we will be subject to a wide array of regulation of the United Kingdom, European Union and United States, in addition to all the regulation of those jurisdictions surrounding new drug development and their manufacture, distribution and use. Compliance will be intricate and costly, partly because of the multiplicity of jurisdictional rules and regulations that have to be followed at the same time. For example, we will be subject to data protection laws and regulations relating to medical records, various medical and general privacy laws, certain environmental laws regarding medical waste, and bribery and corrupt practices law, in addition to all the drug related approval, manufacturing and distribution rules and regulations. | |

| ● | Product liability claims are frequent in the business sector of drug development, especially in connection with novel therapies, and insurance is mandatory and expensive. The inability to obtain insurance may provide product development and claims may surpass our ability to pay and call into question the efficacy of a product with resulting reputational damage. |

| 11 |

| ● | Protecting our intellectual property is paramount in our ability to be able to commercialize our products and generate revenues and investment return for our stockholders. We may not be able to obtain the intellectual property protection we seek due to its cost, requirement to pursue it in many jurisdictions, challenges by others and patent office rejection. | |

| ● | Obtaining and maintaining our patent protection depends on compliance with various procedural, document submission, fee payment and other requirements imposed by governmental patent agencies acting in multiple jurisdictions, and our patent protection could be reduced or eliminated for non-compliance with these requirements. | |

| ● | As part of product development, we may need to license aspects of our research and products from third parties or if our IP is challenged, we may have to seek license accommodation, any of which may be expensive, limited in scope, or unavailable. | |

| ● | We currently have a limited number of employees, and our future success depends on our ability to retain key executives and to attract, retain and motivate qualified personnel at all levels. | |

| ● | We expect to expand our development and regulatory capabilities and potentially implement sales, marketing and distribution capabilities, and as a result, we may encounter difficulties in managing our growth, which could disrupt our operations. We expect to require further funding for these expansions of activity. | |

| ● | We will incur increased costs as a result of operating as a public company in the United States, and our management is required to devote substantial time to new compliance initiatives and corporate governance practices. | |

| ● | Certain of our existing stockholders, members of our board of directors and senior management maintain the ability to exercise significant control over us. Your interests may conflict with the interests of these existing stockholders. | |

| ● | Future sales, or the possibility of future sales, of a substantial number of our ordinary shares could adversely affect the price of our ordinary shares in the market. After any lock up period, a substantial number of our issued and outstanding ordinary shares will be eligible for trading on the public securities market. | |

| ● | As a foreign private issuer, we, and our stockholders, have certain exceptions to disclosure regulation under United States federal securities regulation, and we will take certain NASDAQ governance exceptions. Consequently, investors may not have the totality of disclosure about and governance controls in TCB as compared to United States domestic reporting companies. | |

| ● | Shareholder rights and recourse will be governed by and ultimately determined by Scottish and United Kingdom law and judicial process, which in many ways are more limited than United States law and practice. Most of our directors and officers are not resident in the United States. Most of our assets are located in the United Kingdom. |

| 12 |

Investing in our company and its securities involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this prospectus, including our consolidated financial statements and related notes, before investing in our company and our securities. If any of the following risks materialize, our business, financial condition, operating results and prospects could be materially and adversely affected. In that event, the price or value of our ordinary shares could decline, and you could lose part or all of your investment.

Risks Related to Our Financial Position and Need for Additional Capital

We have incurred net losses every year since our inception and expect to continue to incur net losses in the future and may never achieve profitability.

We have generated losses since our inception in 2013. Since then, we have devoted substantially all of our resources to research and development efforts relating to our genetically unmodified and genetically engineered GDT cell candidates, including engaging in activities to manufacture and supply our GDT cell candidates for clinical trials, conducting initial clinical trials of our lead candidates, general and administrative support for these operations, and protecting our intellectual property. Based on our current plans, we do not expect to generate product or royalty revenues until we obtain marketing approval for, and commercialize, any of our GDT cell-based candidates.

For the fiscal years ended December 31, 2019 and 2020, we incurred net losses of £6.1 million and £5.5 million ($ 7.5 million) respectively. As of December 31, 2020, we had an accumulated deficit of £19.9 million ($ 27.2 million). We expect to continue incurring significant losses as we continue with our research and development programs and to incur general and administrative costs associated with our operations. The extent of funding required to develop our product candidates is difficult to estimate given the novel nature of our GDT cell-based cell therapy candidates and their un-proven route to market. Ultimately, our profitability is dependent upon the successful development, approval, and commercialization of our GDT cell-based therapeutic candidates and achieving a level of revenues adequate to support our cost structure. We may never achieve profitability and until we do, we will continue to need to raise additional cash.

We have never generated any revenue from sales of our GDT cell-based product candidates and our ability to generate revenue from sales of our therapeutic candidates and become profitable depends significantly on our success in a number of factors.

We continue to focus on development activities for our technologies and implementation of the early parts of our business plan. A large percentage of our expenses will continue to be fixed; accordingly, our losses may be greater than expected and our operating results will suffer. We may never achieve commercial success and continue to operate in the research and development stage, without commercially launching any products at this time. We have limited historical financial data upon which we may base our projected revenue and base our planned operating expenses. Our limited operating history makes it difficult for potential investors to evaluate our potential product candidates, drug therapies or prospective operations and business prospects. As a development stage company, we are subject to all the risks inherent in the initial organization, business development, financing, unexpected expenditures, and complications and delays that often occur in a new business. Investors should evaluate an investment in us in light of the uncertainties encountered by developing companies in a competitive environment. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

We have no GDT cell-based therapeutic candidates approved for commercial sale and have not generated any revenue from sales of our GDT cell-based therapeutic candidates, and do not anticipate generating any revenue from sales of our GDT cell-based therapeutic candidates until sometime after we receive regulatory approval, if at all, for the commercial sale of a GDT cell-based therapeutic candidate. We intend to fund future operations through our existing and future collaboration and licensing agreements for other therapeutic targets and through additional equity financings. Our ability to generate revenue and achieve profitability depends on our success in many factors, including:

| ● | completing research regarding, and preclinical and clinical development of, our GDT cell-based therapeutic candidates; | |

| ● | obtaining regulatory approvals and marketing authorizations for our GDT cell-based therapeutic candidates for which we complete clinical trials; | |

| ● | developing sustainable and scalable manufacturing and supply processes for our GDT cell-based therapeutic candidates, including establishing and maintaining commercially viable supply relationships with third parties and pursuing our own commercial manufacturing capabilities and infrastructure; |

| 13 |

| ● | launching and commercializing GDT cell-based therapeutic candidates for which we obtain regulatory approvals and marketing authorizations, either directly or with a collaborator or distributor; | |

| ● | obtaining market acceptance of our GDT cell-based therapeutic candidates as viable treatment options; | |

| ● | addressing any competing technological and market developments; | |

| ● | identifying, assessing, acquiring and/or developing new GDT cell-based therapeutic candidates; | |

| ● | maintaining, protecting, and expanding our portfolio of intellectual property rights, including patents, trade secrets and know-how; and | |

| ● | attracting, hiring and retaining qualified personnel. |

Even if one or more of our GDT cell-based therapeutic candidates is approved for commercial sale, we anticipate incurring significant costs associated with commercializing any approved GDT cell-based therapeutic candidate. Our expenses will increase beyond our current expectations if the U.S. Food and Drug Administration, the FDA, or the United Kingdom Medicines and Healthcare products Regulatory Agency, the MHRA, or any other regulatory agency require changes to our manufacturing processes or assays, or for us to perform preclinical programs and clinical or other types of trials in addition to those that we currently anticipate. If we are successful in obtaining regulatory approvals to market one or more of our GDT cell-based therapeutic candidates, our revenue will be dependent, in part, upon the size of the markets in the territories for which we gain regulatory approval, the accepted price for the GDT cell-based therapeutic candidate, the ability to get reimbursement at any price, and whether we own the commercial rights for that territory. If the number of our addressable disease patients is not as significant as we estimate, the indication approved by regulatory authorities is narrower than we expect, or the reasonably accepted population for treatment is narrowed by competition, physician choice or treatment guidelines, we may not generate significant revenue from sales or supplies of such GDT cell-based therapeutic candidates, even if approved. If we are not able to generate revenue from the sale of any approved GDT cell-based therapeutic candidates, we may never become profitable.

If we fail to obtain additional financing as needed, we may be unable to complete the development and commercialization of our GDT cell-based product candidates.

Our operations have required substantial amounts of cash since inception. We expect to continue to spend substantial amounts to continue the development of our GDT cell-based therapeutic candidates, including for future clinical trials. We expect to use a large part of the net proceeds from this offering to advance and accelerate the clinical development of our therapeutic candidates, therefore, changing circumstances beyond our control may cause us to increase our spending significantly faster than we currently anticipate, we believe we will require additional capital, likely in significant amounts, for the further development and commercialization of our GDT cell-based therapeutic candidates.

We cannot be certain that additional funding will be available on acceptable terms, or at all. We have no committed source of additional capital. If we are unable to raise additional capital in sufficient amounts or on terms acceptable to us, we may have to significantly delay, scale back or discontinue the development or commercialization of our GDT cell-based therapeutic candidates or other research and development initiatives. Our license and supply agreements may also be terminated if we are unable to meet the milestone obligations under these agreements. We could be required to seek collaborators for our GDT cell-based therapeutic candidates at an earlier stage than otherwise would be desirable or on terms that are less favorable than might otherwise be available or relinquish or license on unfavorable terms our rights to our GDT cell-based therapeutic candidates in markets where we otherwise would seek to pursue development or commercialization ourselves. Any of the above events could significantly harm our business, prospects, financial condition and results of operations and cause the price of our ordinary shares to decline.

We, as well as our independent registered public accounting firm, have expressed substantial doubt about our ability to continue as a going concern.

Our recurring losses from operations and negative cash flow raise substantial doubt about our ability to continue as a going concern. As a result, our independent registered public accounting firm included an explanatory paragraph in its report on our financial statements for the years ended December 31, 2019 and 2020 with respect to this uncertainty.

Our

ability to continue as a going concern ultimately is dependent upon our generating cash flow from sales that are sufficient to fund operations

or finding adequate financing to support our operations. To date, we have had no product revenues and relied on equity-based financing

from the sale of securities subscribed by our founders and related parties and in various private placements; and receipts from collaboration

partners. Our research and development plans may not be successful in creating a marketable product, and our business plan may

not be successful in achieving a sustainable business and generating revenues. Although we are engaged in the offering described in this

prospectus, we have no arrangements in place for all the anticipated, required financing to be able to fully implement our business plan.

If we are unable to continue as planned currently, we may have to curtail some or all of our business plan and operations. In such case,

investors will lose all or a portion of their investment.

| 14 |

We anticipate needing additional financing over the longer term to execute our business plan and fund operations, which additional financing may not be available on reasonable terms or at all.

The proceeds from this offering are expected to provide capital to further develop our drug product candidates and fund our overall business plan through late 2022. We will require additional capital in the future to fully develop our technologies and potential products to the stage of a commercial launch. We cannot give now any indication of the amount of future funding that we will need or give any assurance that we will be able to obtain all the necessary funding that we may need. We may pursue additional funding through various financing sources, including the private and public sale of our equity and debt securities, licensing fees for our product candidates, joint ventures with capital partners and project type financing. We also may seek government-based financing, such as development and research grants. There can be no assurance that funds will be available on commercially reasonable terms, if at all. If financing is not available on satisfactory terms, we may be unable to further pursue our business plan and we may be unable to continue operations, in which case you may lose your entire investment. Alternatively, we may consider changes in our business plan that might enable us to achieve aspects of our business objectives and lead to some commercial success with a smaller amount of capital, but we cannot assure that changes in our business plan will result in revenues or maintain any value in your investment.

Exchange rate fluctuations may materially affect our results of operations and financial condition.

Due to the international scope of our operations, our assets, earnings and cash flows are influenced by movements in exchange rates of several currencies, particularly the U.S. dollar, the pound sterling and the euro. Our reporting currency and our functional currency is the pound sterling and the majority of our operating expenses are paid in pound sterling. We regularly acquire services, consumables and materials in U.S. dollars, pound sterling and the euro. Further potential future revenue may be derived from abroad, particularly from the United States. As a result, our business and the price of our ordinary shares may be affected by fluctuations in foreign exchange rates between the pound sterling and these other currencies, which may also have a significant impact on our results of operations and cash flows from period to period. Currently, we do not have any exchange rate hedging arrangements in place.

Risks Related to Development, Clinical Testing and Commercialization of Our Investigational

Therapies and Any Future Therapeutic Candidates

Our GDT cell therapies represent a novel approach to cancer and virus treatment that could result in heightened regulatory scrutiny, delays in clinical development, or delays in or our ability to achieve regulatory approval or commercialization of our therapeutic candidates.

Our products are novel cancer and virus treatment approaches that carry inherent development risks. We are therefore constantly evaluating and adapting our therapeutic candidates following the results obtained during development work and the ongoing clinical trials. Further development, characterization and evaluation may be required, depending on the results obtained, in particular where such results suggest any potential safety risk for patients. The need to develop further assays, or to modify in any way the protocols related to our therapeutic candidates to improve safety or effectiveness, may delay a clinical program, regulatory approval or commercialization, if approved at all, of any therapeutic candidate. Consequently, this may have a material impact on our ability to receive milestone payments and/or generate revenues from our therapeutic candidates. In addition, given the novelty of our GDT cell therapeutic candidates, the end users and medical personnel require a substantial amount of education and training in their administration of our cell therapy. Regulatory authorities have very limited experience with commercial cell therapies for disease treatment. As a result, regulators may be more risk averse or require substantial dialogue and education as part of the normal regulatory approval process for each stage of development of our therapeutic candidates.

GDT cell therapy creates significantly increased risk in terms of side-effect profile, ability to satisfy regulatory requirements associated with clinical trials, and the long-term efficacy of administered cells.

Development of a pharmaceutical or biologic therapy product has inherent risks based on differences in patient population and responses to therapy and treatment. The mechanism of action and impact on other systems and tissues within the human body following administration of GDT cell therapy products is not completely understood, which means that we cannot predict the long-term effects of treatment with the GDT cell therapy product. We are aware that certain patients may not respond to GDT cell therapy and other patients may relapse. The percentage of the patient population in which these events may occur is unknown, but the inability of patients to respond and the possibility of relapse may impact our ability to conduct clinical trials, to obtain regulatory approvals, if at all, and to successfully commercialize our therapeutic products.

Our GDT cell therapeutic candidates and their application are not fully scientifically understood and are still undergoing validation and investigation. The utility of our GDT cell products may depend on persistence, potency, durability and infiltration capacity of the GDT cells within a patient’s body. The level of persistence and the factors affecting such persistence, potency and infiltration capacity in patients are not completely understood, which presents an additional risk to the ongoing development and use of our therapeutic candidates. Certain steps involved in validating and carrying out testing require access to samples (for example tissue samples or cell samples) from third parties. Such samples may be obtained from universities or research institutions and will often be provided subject to satisfaction of certain terms and conditions. There can be no guarantee that we will be able to obtain samples in sufficient quantities to enable development of and use of the full preclinical safety testing program for CAR-T therapeutic candidates undergoing development. In addition, the terms under which such samples are available may not be acceptable to us or may restrict our use of any generated results or require us to make payments to the third parties.

| 15 |

Our products, before they can be commercialized, will require regulatory approval.

We cannot commercialize a product candidate until the appropriate regulatory authorities have reviewed and approved the product candidate. Approval by the FDA, the MHRA and comparable other regulatory authorities is lengthy and unpredictable, and depends upon numerous factors. Approval policies, regulations, or the type and amount of clinical data necessary to gain approval may change during the course of a product candidate’s clinical development and may vary among jurisdictions, which may cause delays in the approval or the decision not to approve an application. We have not obtained commercialization regulatory approval for any product candidate, and it is possible that any of our product candidates will never obtain regulatory approval.

Applications for product candidates we may develop could fail to receive regulatory approval for many reasons, including but not limited to:

| ● | our inability to demonstrate to the satisfaction of the regulatory authorities that a product candidate we develop is safe and effective; | |

| ● | the regulatory authorities may disagree with the design or implementation of our clinical trials; | |

| ● | the population studied in the clinical program may not be sufficiently broad or representative to assure safety in the full population for which we seek approval; | |

| ● | the regulatory authorities’ requirement for additional preclinical studies or clinical trials; | |

| ● | the regulatory authorities may disagree with our interpretation of data from nonclinical studies or clinical trials; | |

| ● | the data collected from clinical trials may not be sufficient to support the submission of a new drug application, or NDA, or other submission for regulatory approval; | |

| ● | we may be unable to demonstrate to the regulatory authorities that a product candidate’s risk-benefit ratio for its proposed indication is acceptable; | |

| ● | the regulatory authorities may fail to approve the manufacturing processes, test procedures and specifications, or facilities of third-party manufacturers with which we contract for clinical and commercial supplies; and | |

| ● | the approval policies or regulations of the regulatory authorities may change in a manner that renders our clinical trial design or data insufficient for approval. |

The lengthy approval process, as well as the unpredictability of the results of clinical trials, may result in our failing to obtain regulatory approval to market a product candidate in the United States, the UK, the EU or elsewhere, which would significantly harm our business, prospects, financial condition and results of operations.

We may encounter substantial delays in completing our clinical trials, which in turn will result in additional costs and may ultimately prevent successful or timely completion of the clinical development and commercialization of our product candidates.

We must conduct extensive clinical trials to demonstrate the safety and efficacy of the product candidates in humans before commercialization. Clinical testing is expensive, time-consuming and uncertain as to outcome. We cannot guarantee that any clinical trials will be conducted as planned or completed on schedule, if at all. A failure of one or more clinical trials can occur at any stage of testing. Events that may prevent successful or timely completion of clinical development include:

| ● | delays in reaching, or any failure to reach, a consensus with regulatory agencies on study design; | |

| ● | delays in obtaining FDA required Institutional Review Board, or IRB, approval at each clinical trial site; | |

| ● | delays in recruiting a sufficient number of suitable patients to participate in our clinical trials; | |

| ● | imposition of a clinical hold by regulatory agencies, after an inspection of our clinical trial operations or study sites; |

| 16 |

| ● | failure by third parties or us to adhere to clinical trial, regulatory or legal requirements; | |

| ● | failure to perform in accordance with good clinical practices, GCP, or applicable regulatory guidelines in other countries; | |

| ● | delays in the testing, validation, manufacturing and delivery of sufficient quantities of our product candidates to the clinical sites; | |

| ● | delays in having patients’ complete participation in a study or return for post-treatment follow-up; | |

| ● | clinical trial sites or patients dropping out of a trial; | |

| ● | delay or failure to address any patient safety concerns that arise during the course of a trial; | |

| ● | unanticipated costs or increases in costs of clinical trials of our product candidates; | |

| ● | occurrence of serious adverse events associated with the product candidate that are viewed to outweigh its potential benefits; or | |

| ● | changes in regulatory requirements and guidance that require amending or submitting new clinical protocols. |

We

could also encounter delays if a clinical trial is suspended or terminated by us or by regulators and related reviewing authorities such

as IRBs of the institutions in which such trials are being conducted, by an independent Safety Review Board. Suspension or termination

of a clinical trial might be due to a number of factors, including failure to conduct the clinical trial in accordance with regulatory

requirements or our clinical protocols, inspection of the clinical trial operations or trial site resulting in the imposition of a clinical

hold, unforeseen safety issues or adverse side effects, or failure to demonstrate a benefit from using a therapy. In addition, if we

make manufacturing or formulation changes to our product candidates, we may need to conduct additional studies to bridge our modified

product candidates to earlier versions. In addition, any delays in completing our clinical trials will increase our costs, slow down

our product candidate development and approval process and jeopardize our ability to obtain regulatory approvals, commence product sales

and generate revenues. Any of these occurrences may significantly harm our business, prospects, financial condition and results of operations.

Manufacturing and administering our GDT cell-based therapeutic candidates is complex, and we may encounter difficulties in production, particularly with respect to process development or scaling-up of our manufacturing capabilities. If we encounter such difficulties, our ability to supply of our GDT cell therapeutic candidates for clinical trials or for commercial purposes could be delayed or stopped.

Manufacturing and administrating our GDT cell-based therapeutics candidates is complex and highly regulated. The manufacture process of our GDT cell-based therapeutics involves complex processes, including peripheral blood mononuclear cell isolation from leukapheresis material, stimulation of the GDT cells, expansion of the cells to obtain a desired dose, and ultimately infusion of the cells to the patient’s body. On occasions the GDT cell therapeutic could be genetically modified, which could involve manufacturing of lentiviral vectors containing the gene of our interest (for example Chimeric Antigen Receptor) and transducing the cells or a method such as electroporation or nucleofection of a plasmid containing the gene of interest to the cells. As a result of the complexities, our manufacturing and supply costs are likely to be higher than those in more traditional manufacturing processes and the manufacturing process is less reliable and more difficult to reproduce. Our manufacturing process is, and will be, susceptible to product loss or failure due to logistical issues, including manufacturing issues associated with the differences in patients’ white blood cells, interruptions in the manufacturing process, contamination, equipment or reagent failure, supplier error and variability in GDT cell-based therapeutic candidate and patient characteristics. Even minor deviations from normal manufacturing processes could result in reduced production yields, product defects, and other supply disruptions. If microbial, viral or other contaminations are discovered in our GDT cell-based therapeutic candidates or in the manufacturing facilities in which our GDT cell based therapeutic candidates are made or administered, the manufacturing facilities may need to be closed for an extended period of time to investigate and remedy the contamination. As our GDT cell-based therapeutic candidates progress through preclinical programs and clinical trials towards approval and commercialization, it is expected that various aspects of the manufacturing and administration process will be altered in an effort to optimize processes and results.

We have identified some improvements to our manufacturing and administration processes, but these changes may not achieve the intended objectives, and could cause our GDT cell-based therapeutic candidates to perform differently and affect the results of planned clinical trials or other future clinical trials. The changes may require amendments to be made to regulatory applications which may further delay the timeframes under which modified manufacturing processes can be used for any GDT cell-based therapeutic candidate. For example, we are planning to introduce automated enclosed systems to our production process. This will require development work to ensure that these modifications do not alter the characteristics of the product. If the GDT cell-based therapeutic candidate manufactured under the new process has a worse safety or efficacy profile than the prior investigational product, we may need to re-evaluate the use of that manufacturing process, which could significantly delay the progress of our clinical trials.

| 17 |

Developing a commercially viable process is a difficult and uncertain task and there are risks associated with scaling to the level required for advanced clinical trials or commercialization, including, among others, increased costs, potential problems with process scale-out, process reproducibility, stability issues, lot consistency, and timely availability of reagents or raw materials. We may ultimately be unable to reduce the expenses associated with our GDT cell-based therapeutic candidates to levels that will allow us to achieve a profitable return on investment. If we are unable to demonstrate that our commercial scale product is comparable to the product used in clinical trials, we may not receive regulatory approval for that product without additional clinical trials. Even if we are successful, our manufacturing capabilities could be affected by increased costs, unexpected delays, equipment failures, labor shortages, natural disasters, power failures and numerous other factors that could prevent us from realizing the intended benefits of our manufacturing strategy, which in turn could have a material adverse effect on our business.

We may seek expedited approval in the European Union and United States for our therapeutic candidates, but we may not be able to obtain or maintain such designation.